Do any companies have a great central location where they keep track of projects/activities/areas of ownership, who owns them, and the status/links to progress? Looking for examples of how this is done really well.

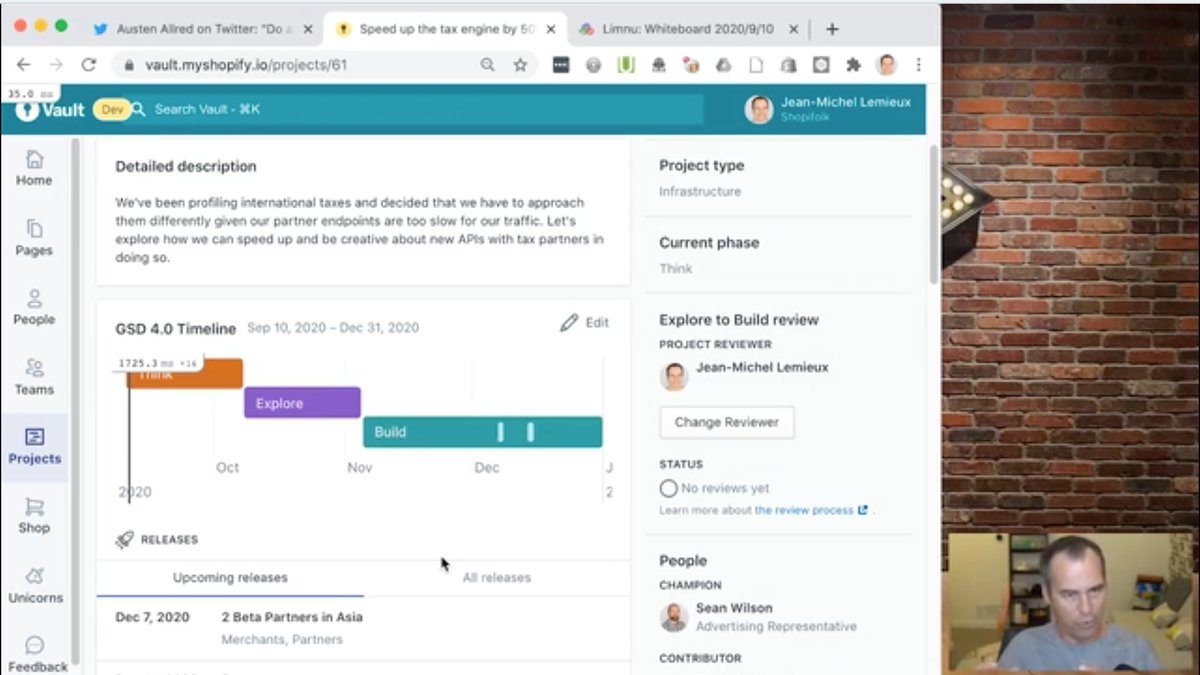

Hey @Austen, here's a scrappy / non-polished demo of the "why" and "what" of how we collab and track what we work on at Shopify. I tried to tweet thread, but it's easier to explain on video. Happy to take questions 👇🏼👇🏼 vimeo.com/456735890 pic.twitter.com/Sp2JW83VMZ twitter.com/Austen/status/…

I know it's fashionable to do super lightweight research these days - e.g. 'no report, do the analysis in miro and move on' But this enormously limits the shelf life of your work.

💰 Highest paying remote companies in Aug: 1 🐀@carted $175k 2 📋@smart_contract 150k 3 🚑@doximity_tech $135k 4 ⚛️@toptal $130k 5 🐍@tucows $125k 6 ♾️@shorthand $120k 7 🚥@safetywing $120k 8 🐘@soflyy $120k 9 👨🏫@aula_education $115k *median pay remoteok.io/remote-work-st…

anyone know a really great brand designer? (branding, logos, iconography, site design in figma, etc.) Recommendations wanted! Freelance / not huge agency preferred. Thx!

[THREAD] I know this problem happens often... A founder wants to create a product but can't find a good domain name. I've always joked that it's the most difficult part of building a product. 😂 But it's not too hard — here are some creative ways to find a solid domain name:

What is your go-to article that defines "MVP" ... that if everyone could read and understand that post, we'd stop arguing about what MVP means? Links please!

Any recommendations for a good guide on helping people through the transition from a sync/meeting culture to an async/documentation culture?

anyone make a shift to more writing-centric collaboration during the pandemic (away from, say, presentations or facilitated synchronous conversations)? lessons learned? mistakes to avoid?

Always add TLDR

Make Skimmable

Don't just write make Flow charts

a strategy always exists bc ppl have beliefs and assumptions about the future, their role in it, and their ability (or lack thereof) to shape it, "cause" it, or respond to it. whether it is plausible, "good", etc. is another question starting point: map beliefs & assumptions